San Luis Trust Bank is shut down by regulators

Financially troubled San Luis Trust Bank, founded in 1999 and once lauded as one of the nation’s top community banks, was forced into federal receivership Friday.

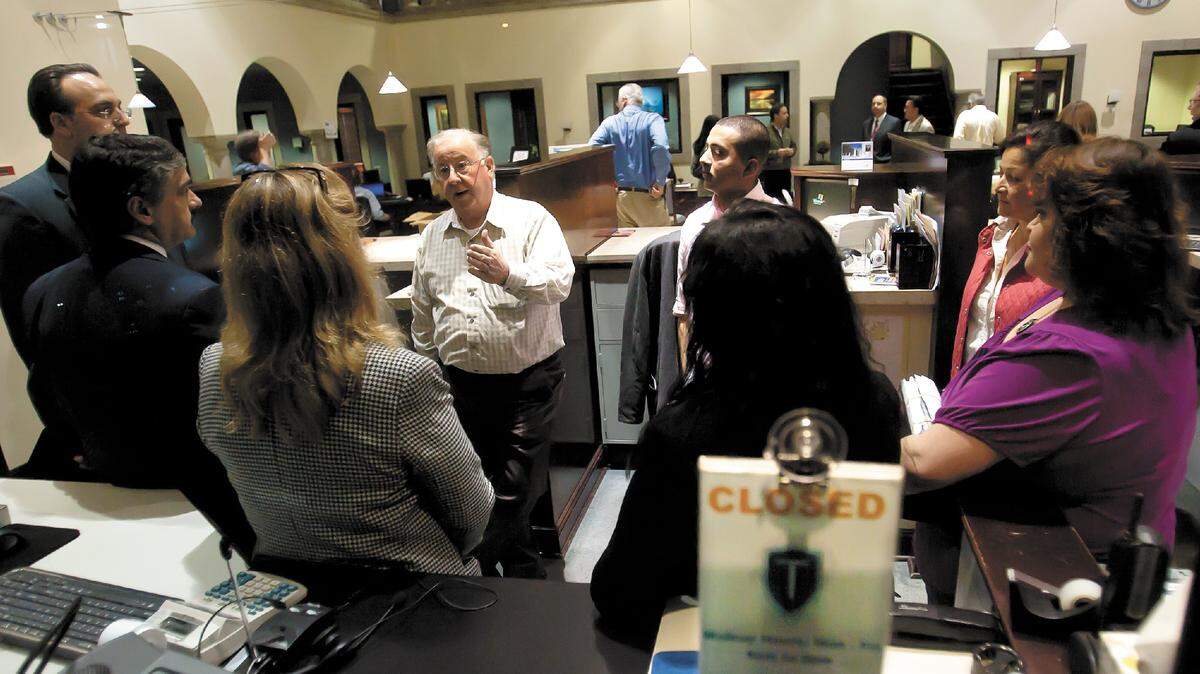

The single-office bank at 1001 Marsh St. will reopen Tuesday as First California Bank of Westlake Village. Monday is a bank holiday.

San Luis Trust depositors can continue to access accounts over the three-day weekend as before, by writing checks or using ATM or debit cards. Checks drawn on the bank will continue to be processed. Loan customers should continue to make payments as usual.

Customers should use the Marsh Street location until First California Bank advises them that they can process their accounts at other First California branches.

The Office of Thrift Supervision closed San Luis Trust at the end of the business day Friday, after finding that it was critically undercapitalized, and appointed the Federal Deposit Insurance Corp. as receiver. A bank’s capital (assets minus liabilities) provides a cushion against losses.

FDIC representative Barbara Brunson said San Luis Trust was “heavily invested in real estate transactions and loans,” suggesting that the economic crisis contributed to the bank’s decline.

A dozen FDIC agents in suits gathered across the street from the bank just after 6 p.m. Friday, holding suitcases and sipping coffee under umbrellas before entering the bank together.

About 60 Irvine-based FDIC agents will work 12-hour days this weekend at the bank and a remote location to facilitate the transition.

First California CEO C.G. Kum told The Tribune that he views the acquisition as a “tremendous asset” and an initial foray into banking on the Central Coast. “This is not where we are going to stop,” he said.

Kum plans to hire a local person to fill a newly created position of regional president for the branch. He added that the bank will keep as many San Luis Trust employees as possible but noted that some will lose their jobs.

First California was one of two banks to bid on San Luis Trust Bank. It will become First California’s 19th branch and its first branch north of Ventura County, increasing First California’s total assets to $1.9 billion, Kum said.

Terms of transaction

First California Bank will assume all of the deposits of San Luis Trust and essentially all of the assets.

In arranging the sale, the FDIC entered a loss-share transaction with First California Bank on $241.7 million of San Luis Trust’s assets — essentially agreeing to share in loan losses that may be incurred by First California because of nonperforming loans in the local bank’s portfolio.

The FDIC estimates it will absorb $96.1 million in losses, adding that First California Bank’s acquisition of San Luis Trust was the least costly resolution.

As of Dec. 31, San Luis Trust had about $332.6 million in assets and $272.2 million in deposits. Friday’s action follows a Feb. 9 “prompt corrective action” order by OTS — a division of the U.S. Department of Treasury and the primary regulatory body overseeing savings banks — mandating that San Luis Trust increase its capital by Tuesday or face seizure. In January, regulators had denied San Luis Trust’s capital restoration plan.

Since the deadline lapsed Tuesday, Sam Collins, president of San Luis Trust, has not responded to The Tribune’s requests for comment.

San Luis Trust reported a $5.7 million loss in the third quarter, compared with a $3.3 million loss in the same period last year.

It is the 22nd FDIC-insured institution to fail nationwide this year and the third in California. Los Padres Bank, based in Solvang with an office in San Luis Obispo, was closed Aug. 20 and reopened as Pacific Western Bank.

Troubled history

San Luis Trust had been scrutinized by the OTS since 2001, two years after it opened, when it found the bank’s practices “to be unsafe and unsound and inconsistent with prudent operations,” and to “have resulted in violations of law or regulation.”

A cease-and-desist order was issued by regulators in November 2009, which requested that San Luis Trust strengthen its capital ratios, maintain adequate short-term and long-term liquidity, revise its policies for modifying loans and reduce its level of classified assets — typically loans for which payments are not being received on time.

The Tribune reported at the time that the bank had complied with the regulators’ request. Chief Financial Officer Brad Lyon, who was the bank president at the time, said then that the bank’s performance had been affected by continued loan loss provisions and short sales.

Lyon said the bank, like many other institutions, “has not been immune to the unprecedented challenges facing the economy and real estate markets.”

In June 2006, The Independent Banker Magazine, a trade journal, ranked San Luis Trust eighth out of 2,477 banks in its returns on assets and 18th overall on its returns on shareholders’ equity.

That same year, San Luis Trust agreed to make changes to its operations after regulators examined its lending practices, stipulating that the bank no longer make loans to its officers, directors or principal shareholders.

At that time, Lyon said: “We’ve always had philosophical differences with our regulators.”

This story was originally published February 18, 2011 at 6:32 PM with the headline "San Luis Trust Bank is shut down by regulators."